Choices Delta Defined

For instance, ought to a inventory choice value enhance in value by 0.5c with a 1c enhance within the underlying inventory value then the choice has a delta of 0.5.

One other method of delta is because the likelihood of the choice expiring within the cash.

A number of the delta impartial methods are ATM Lengthy Straddle, Lengthy Strangle and calendar unfold.

Choices Delta Math

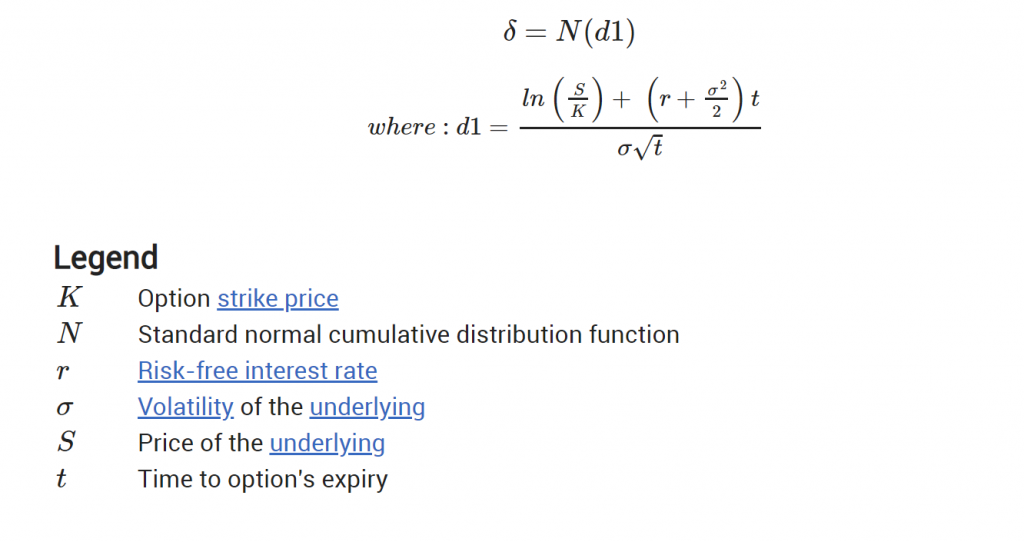

It is not needed to know the maths behind delta (please be happy to go to the following part if you would like), however for these delta is outlined extra formally because the partial spinoff of choices value with respect to underlying inventory value.

The method is beneath (some information of the conventional distribution is required to know it).

Delta is superficially essentially the most intuitive of the choices greeks. Even the most recent newbie would count on the value of an choice, giving the precise to purchase or promote a very safety, to vary with the safety’s value.

Let’s take a look at an instance with name choices on a inventory with $120 inventory value because it rises increased (by $10 to $130, say).

Within the cash choices – these with a strike value lower than $120 – would turn out to be much more within the cash. Thus their worth to the holder would enhance – the likelihood of them remaining within the cash can be increased – and therefore, all different issues being equal, the choice value would rise.

Out of the cash and on the cash choices – these with an train value of $120 or better – would additionally rise in worth. The likelihood of, say, a $140 choice expiring within the cash can be increased if the inventory value was $130 in comparison with $120. Therefore its worth can be increased.

Comparable arguments can be utilized with put choices: their worth rises/falls with the autumn/rise of the underlying (the one distinction being put choices have detrimental delta versus name choices, whose delta is optimistic).

However the extent of this sensitivity – i.e. delta – and the way it pertains to expiration size, value, and volatility is sort of refined. Let’s take a look at it in additional element.

Delta for Quick vs. Lengthy Choices

Choices could be purchased or offered. Relying on which aspect of an choice commerce an investor is on, the delta of that choice will regulate accordingly.

For lengthy choices, delta values are optimistic for calls and detrimental for places. A purchased (lengthy) name may have a delta between 0 and +1, rising as the choice turns into extra in-the-money. A bought put choice may have a delta between 0 and -1, with delta falling the additional the put is positioned in-the-money.

The inverse is true for shorting choices. When promoting name choices, delta scores can be a detrimental worth, between 0 and -1. That is true as a result of a brief name choice place will enhance in worth because the underlying safety falls – the author of a name choice will profit because the underlying safety falls. The opposite method to take a look at that is to know {that a} name choice has a optimistic delta, however that the vendor/author of that decision choice has the inverse publicity.

Equally, put choices, which give a delta publicity of -1 to 0 for the proprietor, expose the vendor/author of the put choice to a optimistic delta between 0 and +1.

How Does Choices Delta Change Over Time?

The impact of time on delta depends upon an choice’s ‘moneyness’.

Within the cash

All different issues being equal, lengthy dated within the cash choices have a decrease delta than shorter dated ones.

Within the cash choices have each intrinsic (inventory value much less train value) and extrinsic worth.

As time progresses the extrinsic reduces (because of theta) and the intrinsic worth (which strikes consistent with inventory value) turns into extra dominant. And so the choice strikes extra consistent with the inventory, and therefore its delta rises in the direction of 1 over time.

Out of the cash

All different issues being equal, quick dated OTM/ATM choices have a decrease delta than longer dated ones.

A brief dated out of the cash choice (particularly one which is considerably OTM) is unlikely to run out within the cash, a reality that’s unlikely to vary with a 1c change in value. Therefore its delta is low.

Longer dated OTM (Out Of The Cash) choices usually tend to expire within the cash – there’s a longer time for the choice to maneuver ITM (In The Cash) – and therefore their worth do transfer with inventory value. Therefore their delta is increased.

On the cash

There is no such thing as a impact of time on the delta of an on the cash choice.

How Does Choices Delta Change With Implied Volatility?

Once more the impact of implied volatility modifications on delta depends upon moneyness.

In The Cash

As we noticed above within the cash choices’ worth comprise each intrinsic and extrinsic quantities.

Usually the upper the proportion of an choice’s worth that’s intrinsic (which strikes precisely consistent with inventory value) and extrinsic worth (which doesn’t), the upper its delta.

Will increase in IV enhance the extrinsic worth of an choice and so, as intrinsic worth isn’t affected by implied volatility, will increase the proportion of the choice’s worth that’s extrinsic. This resultant discount within the intrinsic worth as a proportion of the entire, reduces the choice’s delta as above.

Out Of The Cash

Out of the cash choices have solely extrinsic worth, which is pushed by the likelihood of it expiring within the cash.

A better volatility suggests there’s a better probability of the choice expiring ITM (because the inventory is anticipated to maneuver round extra) and therefore delta will increase.

On the cash

ATM choices have a delta of approx. 0.5, which is unchanged as volatility modifications.

Impact Of Adjustments Of Value On Delta

One of many different subtleties of delta is that it in itself modifications worth because the underlying safety’s value modifications.

The extent to which this happens is one other of the choices greeks: gamma. That is the change in delta leading to in a 1c change in inventory value.

Gamma for lengthy choices holders is optimistic whereas it’s detrimental for brief positions, which means it helps the previous and penalises the latter. Additionally it is at its highest absolute worth close to expiration. (See right here for extra dialogue on gamma).

Conclusion

Delta is a crucial greek because it displays an choice holder’s publicity to one of many foremost variables: the value of the underlying safety.

While one of many best choice ideas to know, its conduct ensuing from modifications to different variables equivalent to time, IV and underlying value is extra advanced.

It’s important for an choices dealer to know these ideas.

In regards to the Creator: Chris Younger has a arithmetic diploma and 18 years finance expertise. Chris is British by background however has labored within the US and recently in Australia. His curiosity in choices was first aroused by the ‘Trading Options’ part of the Monetary Occasions (of London). He determined to deliver this information to a wider viewers and based Epsilon Choices in 2012.

Associated articles:

{kind=link}